Big Banks Make Significant Improvements, Closing the Customer Satisfaction Gap with Regional and Midsize Banks

Overall Customer Satisfaction with Retail Banks Improves Significantly

WESTLAKE VILLAGE, Calif.: 18 April 2013 — Overall customer satisfaction with retail banks improves significantly from 2012, largely a result of improvements made by big banks1, according to the J.D. Power and Associates 2013 U.S. Retail Banking Satisfaction StudySM released today.

The eighth annual customer satisfaction study is the longest-running and most in-depth survey of the retail banking industry, with feedback from more than 50,000 consumers covering various aspects of their banking experience. The study measures satisfaction in six factors: account information; channel activities; facility; fees; problem resolution; and product offerings. Banks are ranked based on overall customer satisfaction in each of the following regions: California, Florida, Mid-Atlantic, Midwest, New England, North Central, Northwest, South Central, Southeast, Southwest and Texas.

After several years of relatively minor increases in overall satisfaction scores, customer satisfaction in 2013 (763 on a 1,000-point scale) has increased by 10 index points from 2012. The largest increase in satisfaction is in the big banks segment, which has improved in 2013 by 16 points from 2012 (759 vs. 743, respectively). While as a group big banks have historically trailed smaller banks in satisfying customers by a fair margin, the satisfaction gap between big banks vs. midsize (785, up 4 points from 2012) and regional (760, up one point from 2012) banks has narrowed year over year.

"While big banks have traditionally had an advantage over smaller banks in terms of convenience of branch locations and technology, their disadvantage was often in the personal service customers desired," said Jim Miller, senior director of banking at J.D. Power and Associates. "Many of the big banks have made great strides in listening to what their customers are asking for: reducing the number of problems customers encounter and, more importantly, improving satisfaction with fees. Consumers today are likely to find banks of all sizes offering the level of convenience, technology and personal service they have come to expect."

During the past several years, many banks have eliminated free checking and implemented new fees, which has often negatively impacted overall satisfaction. The study finds that as fees have begun to stabilize and banks have helped their customers better understand their fee structures, satisfaction in this area has begun to rebound, and is up by 14 points this year from 2012. One-third (33%) of customers say they "completely" understand their fee structure, compared with 26 percent in 2012. Fees also have been a major source of customer problems and complaints. The stability in fees, coupled with banks placing more emphasis on preventing problems, has lowered the proportion of customers experiencing a problem by 3 percentage points year over year, to 18 percent in 2013.

While customers appreciate the personal service they receive at their branch, such transactions are slowly declining, while the numbers of online, ATM and mobile banking transactions are increasing. This trend is especially pronounced in mobile banking, where usage has increased to 17 percent, up from 11 percent in 2012, and the average number of transactions per customer has increased to 51 per year, up from 29 in 2012. As banks roll out envelope-free ATM deposits and deposits by mobile phone, customers are finding it easier to handle routine transactions without needing to visit their branch.

"Successful banks are not pushing customers out of the branch, but rather providing tools that make it easier to conduct their banking business when and where it is convenient for them," said Miller. "Customers are quickly adopting mobile banking, making it a critical service channel for banks, not just a 'nice to have' option."

J.D. Power and Associates offers the following tips for consumers to keep in mind when shopping for a new bank:

- Make sure to review your current bank's fee structure, as well as those of its competitors, to ensure the services and products you're receiving are those that best meet your needs.

- Think about how you want to conduct business with your bank. If personal service is most important to you, how are you treated when you walk into a branch? If you prefer to deal with your bank remotely, what type of mobile and online tools do they offer? With a little research, you can find banks that offer the best of both worlds.

- Evaluate the products and extra services you receive from your bank--including discounts or rewards programs--to ensure they are ones that meet your needs.

- Consider how often you experience problems with your bank, including how well your bank resolves problems and complaints.

- Consider changing banks if you are not satisfied with the service you currently receive. Switching banks may be easier than you think, and most banks have staff dedicated to supporting new customers who have recently switched.

The study measures satisfaction among banks in 11 regions. Study results by region are:

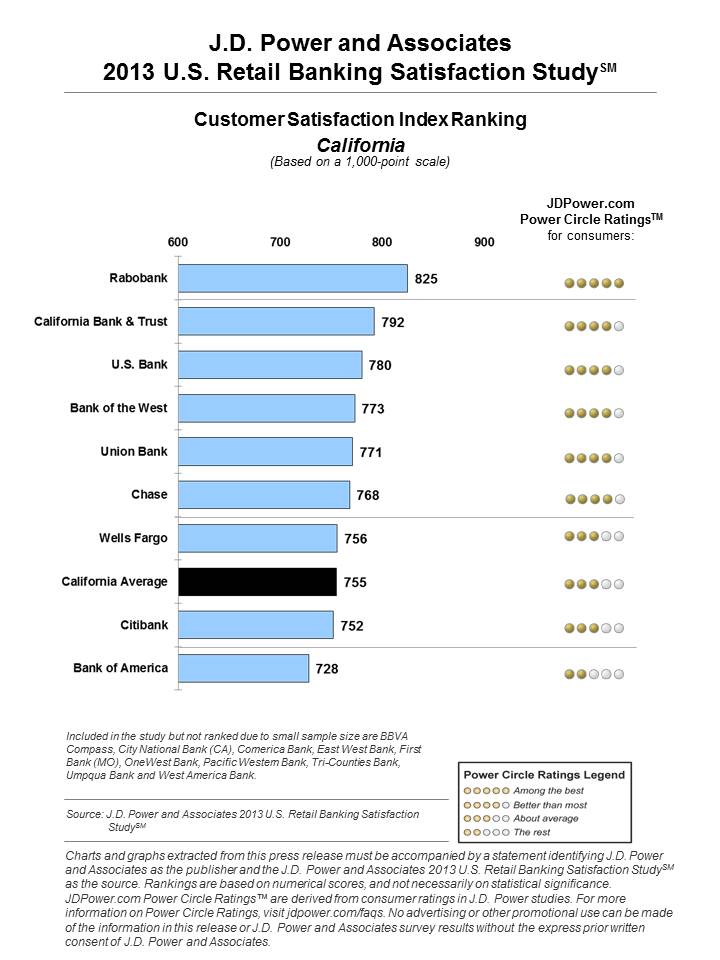

California Region: Rabobank ranks highest in the California region with a score of 825, and performs particularly well in the product offerings, facility, account information, fees and channel activities factors. California Bank & Trust (792) and U.S. Bank (780) follow in the rankings.

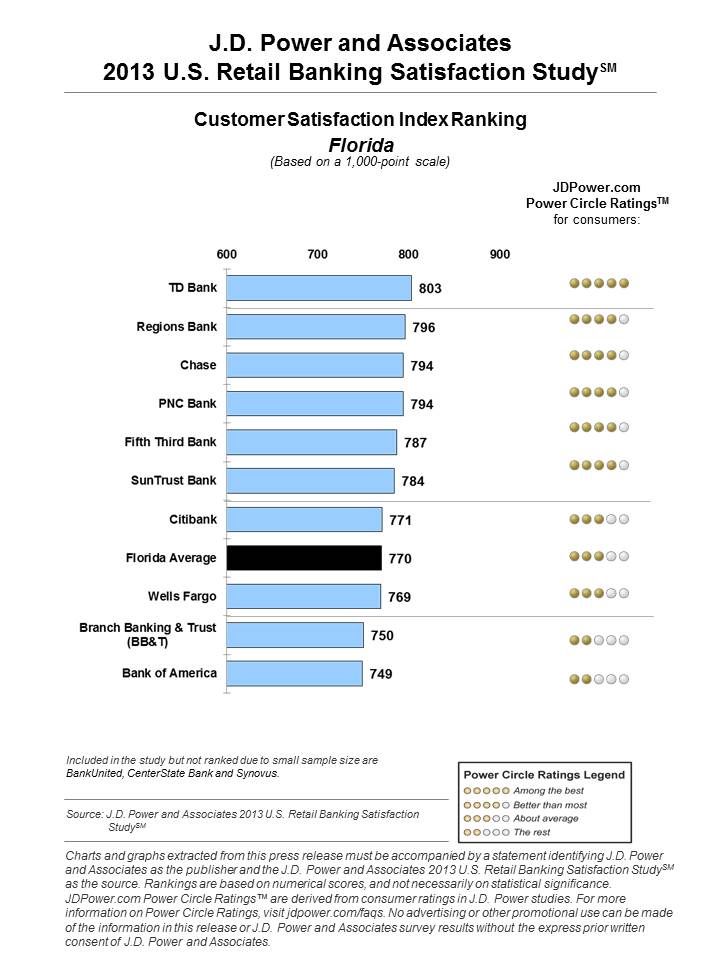

Florida Region: TD Bank ranks highest in the Florida region with a score of 803, performing particularly well in the facility factor. Following TD Bank in the rankings are Regions Bank (796) and Chase and PNC Bank in a tie (794 each).

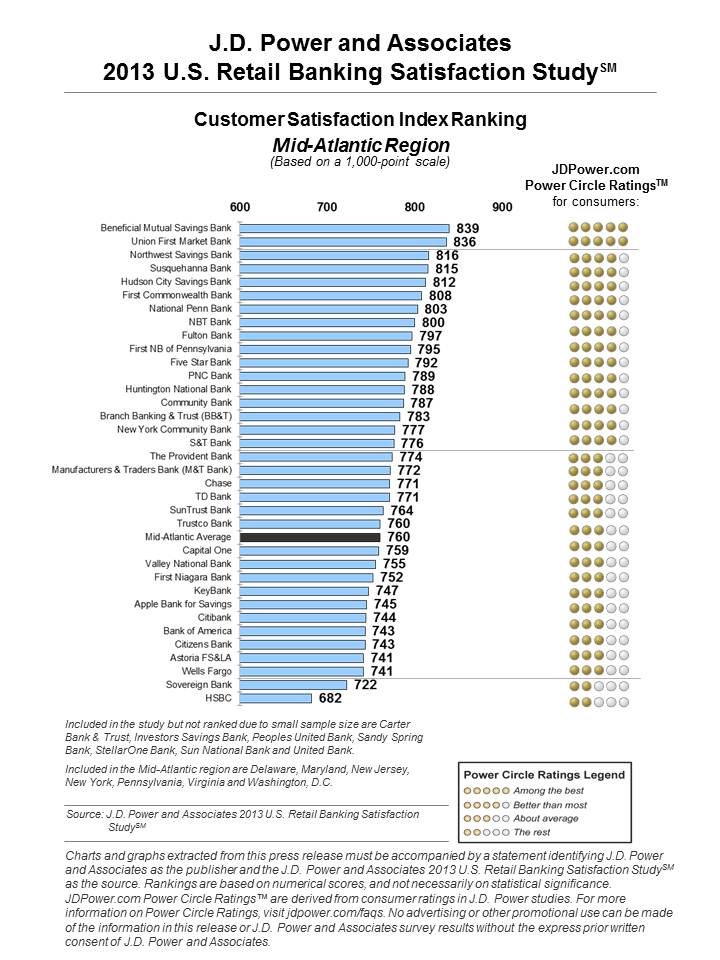

Mid-Atlantic Region: Beneficial Mutual Savings Bank ranks highest in the region with a score of 839, and performs particularly well in the product offerings, account information and channel activities factors. Union First Market Bank (836) and Northwest Savings Bank (816) follow in the rankings.

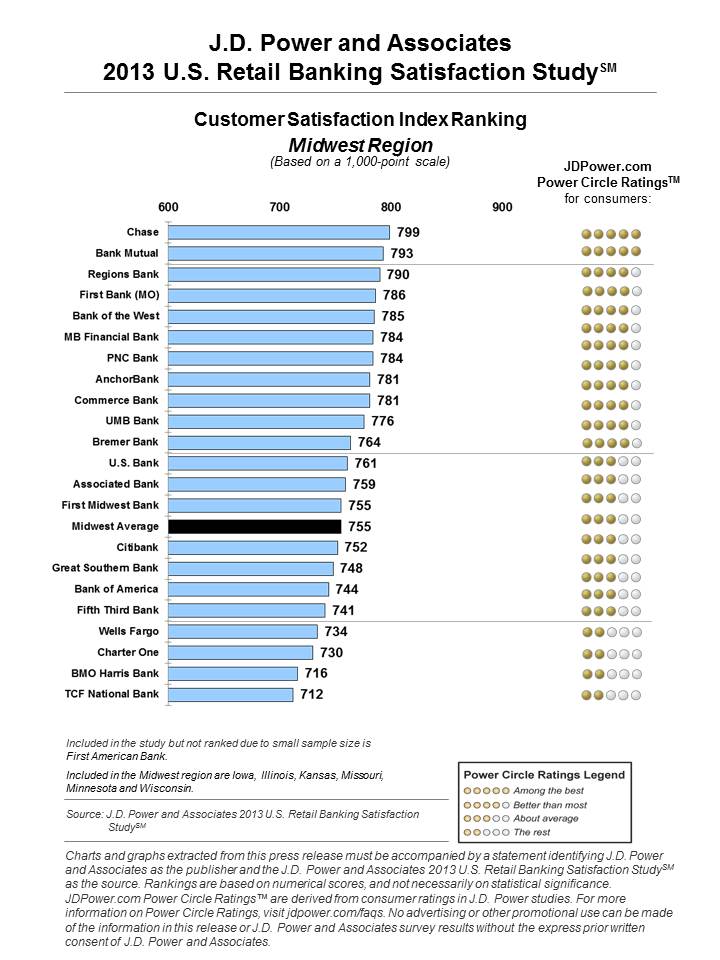

Midwest Region: Chase ranks highest in the region with a score of 799, and performs particularly well in the product offerings, facility and account information factors. Bank Mutual (793) and Regions Bank (790) follow in the rankings.

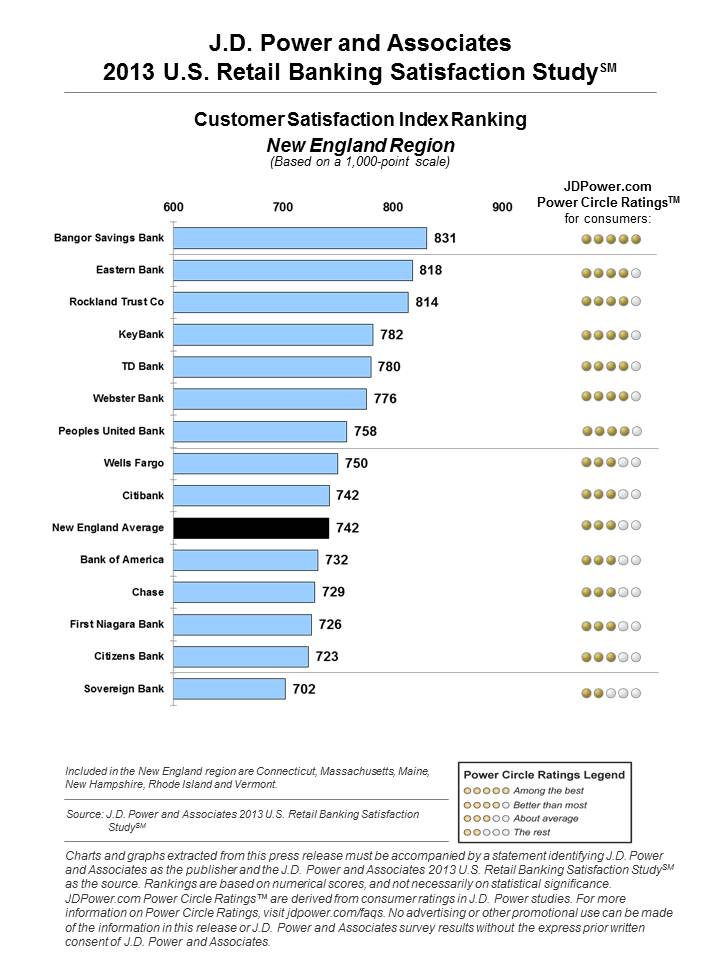

New England Region: Bangor Savings Bank ranks highest in the region with a score of 831, and performs particularly well in the product offerings, fees, and channel activities. Eastern Bank (818) and Rockland Trust Co. (814) follow in the rankings.

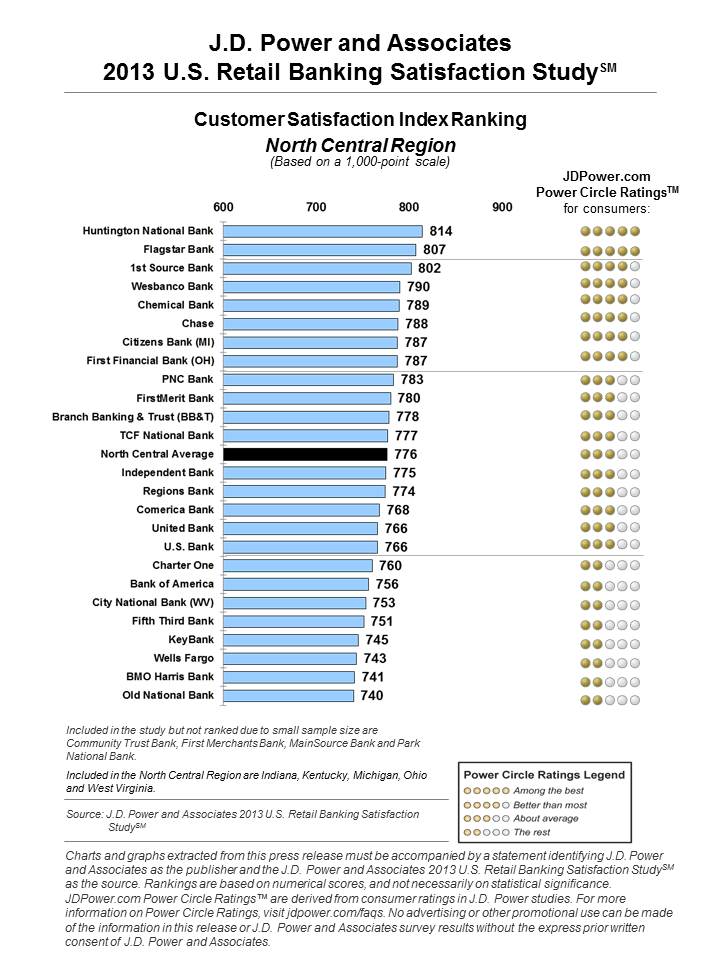

North Central Region: With a score of 814, Huntington National Bank ranks highest in the region, performing particularly well in the account information, fees and channel activities factors. Following in the rankings are Flagstar Bank (807) and 1st Source Bank (802).

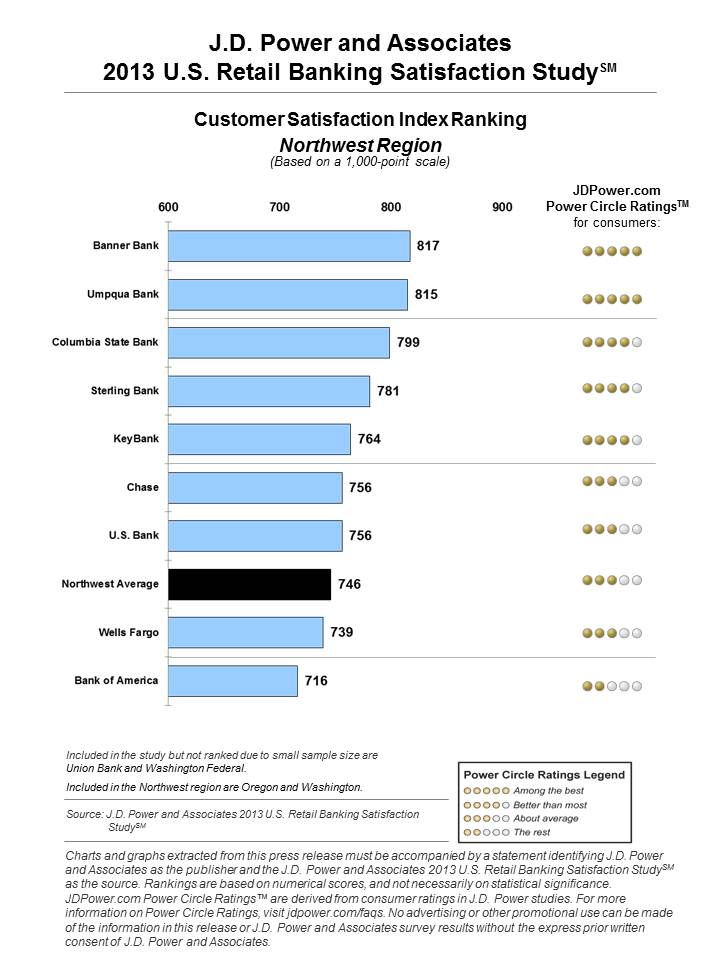

Northwest Region: Banner Bank ranks highest in the region with a score of 817, and performs particularly well in the account information, and fees. Umpqua Bank (815) and Columbia State Bank (799) follow in the rankings.

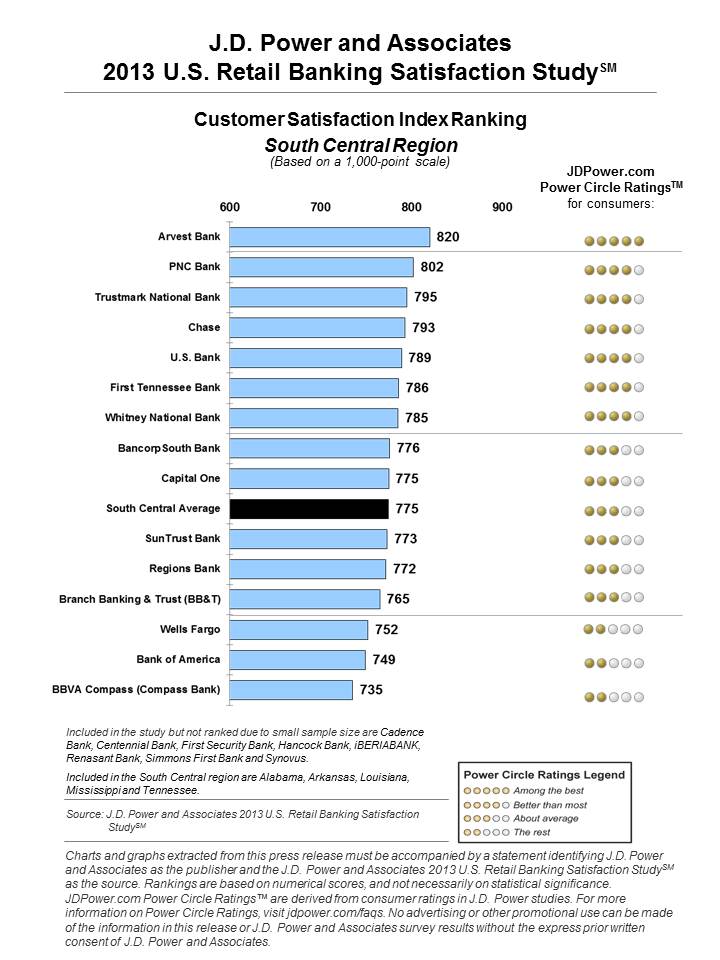

South Central Region: Arvest Bank ranks highest in the region with a score of 820, performing particularly well in the product offerings, facility, account information and channel activities factors. Following in the rankings are PNC Bank (802) and Trustmark National Bank (795).

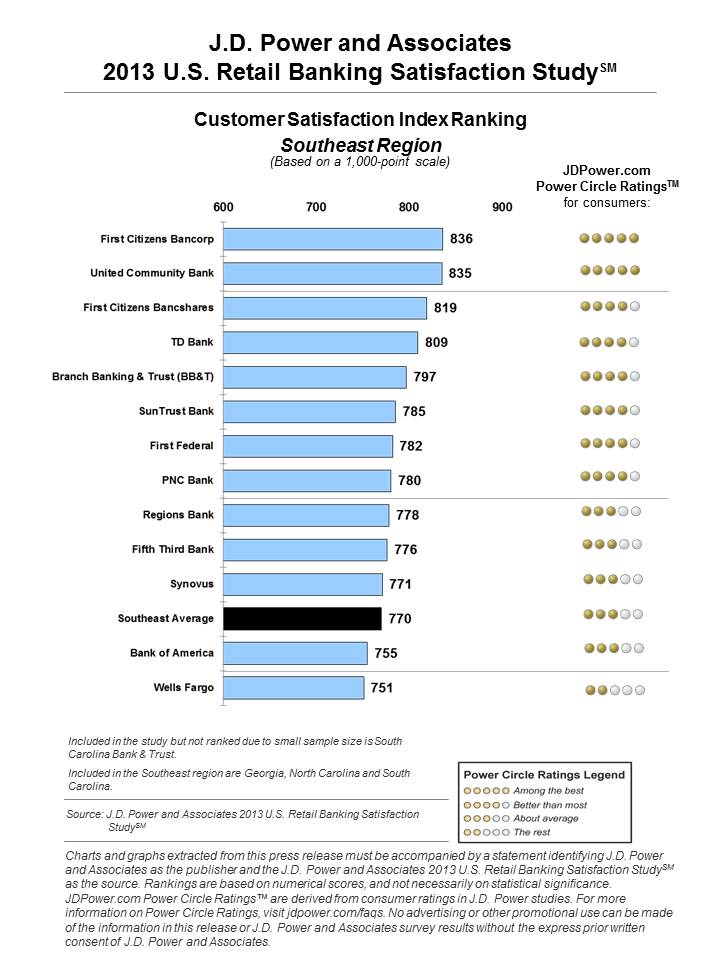

Southeast Region: First Citizens Bancorp ranks highest in the region with a score of 836, and performs particularly well in the product offerings, fees and channel activities factors. United Community Bank (835) and First Citizens Bancshares (819) follow in the rankings.

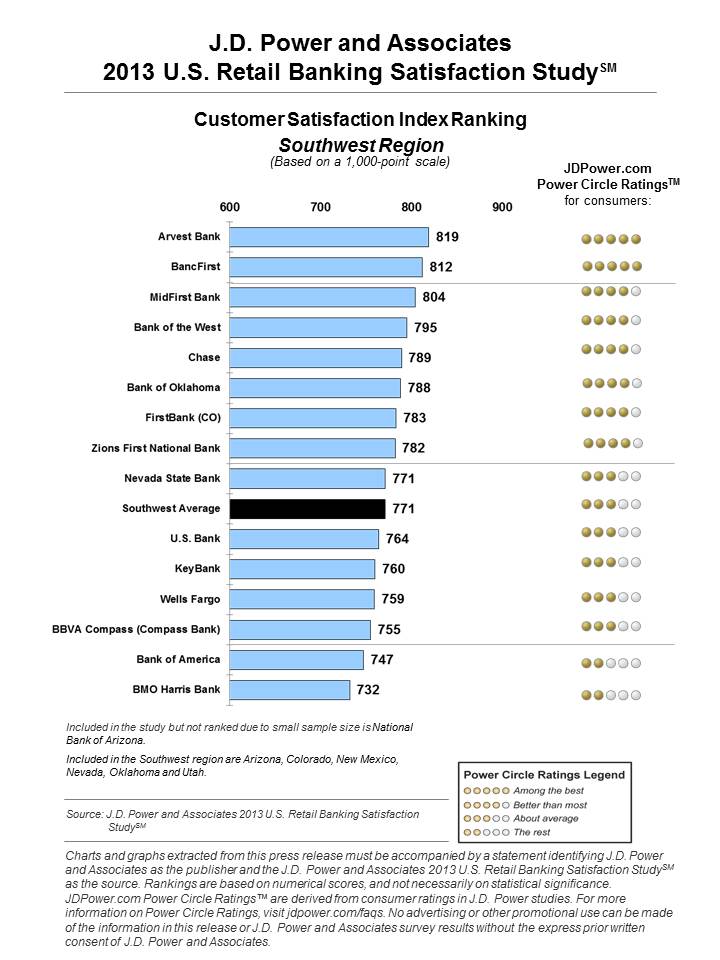

Southwest Region: With a score of 819, Arvest Bank ranks highest in the region, performing particularly well in the product offerings, facility, account information, channel activities and problem resolution factors. BancFirst (812) and MidFirst Bank (804) follow in the rankings.

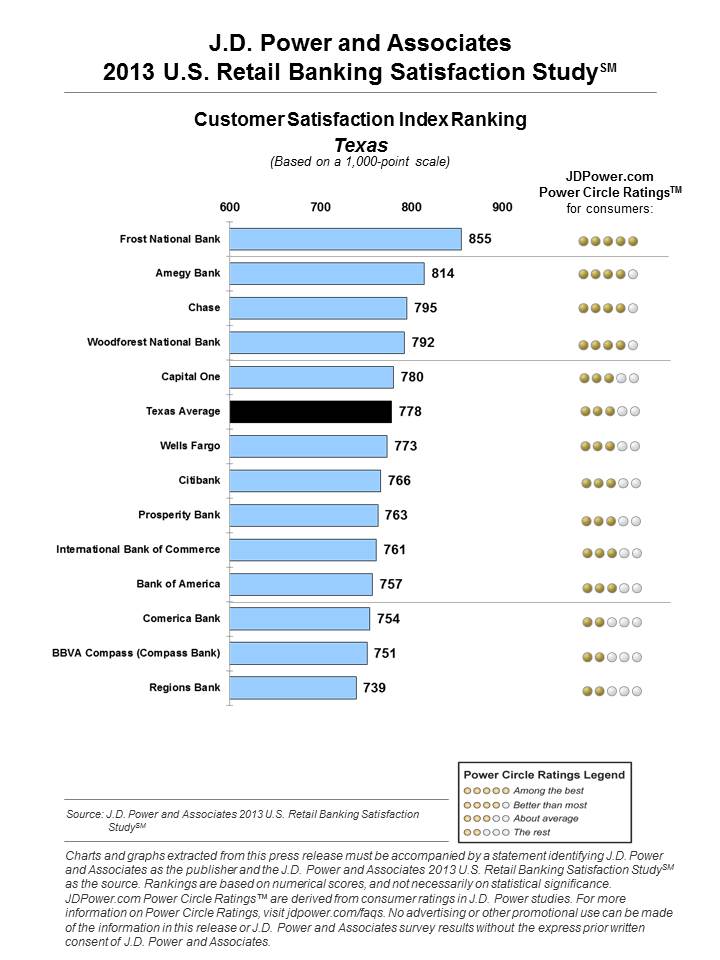

Texas Region: Frost National Bank ranks highest in the Texas region with a score of 855, and performs particularly well in the product offerings, account activities, fees, account information and facility factors. Amegy Bank (814) and Chase (795) follow in the rankings.

The 2013 U.S. Retail Banking Satisfaction Study is based on responses from nearly 52,000 retail banking customers of more than 120 of the largest banks in the United States regarding their experiences with their retail bank. The study was fielded in January and February 2013.

For more information, view retail banking satisfaction rankings at JDPower.com.

1 Big banks are defined as the six largest financial institutions based on total deposits as reported by the FDIC, averaging $180 billion and above. Regional banks are defined as those with between $180 billion and $33 billion in deposits. Midsize banks are defined as those with between $33 billion and $2 billion in deposits.

About J.D. Power and Associates

Headquartered in Westlake Village, Calif., J.D. Power and Associates is a global marketing information services company providing forecasting, performance improvement, social media and customer satisfaction insights and solutions. The company's quality and satisfaction measurements are based on responses from millions of consumers annually. For more information on car reviews and ratings, car insurance, health insurance, cell phone ratings, and more, please visit JDPower.com. J.D. Power and Associates is a business unit of The McGraw-Hill Companies.

About The McGraw-Hill Companies

The McGraw-Hill Companies, to be renamed McGraw Hill Financial (subject to shareholder approval), is a powerhouse in credit ratings, benchmarks and analytics for the global capital and commodity markets. Leading brands include: Standard & Poor's Ratings Services, S&P Capital IQ, S&P Dow Jones Indices, Platts, CRISIL, J.D. Power and Associates, McGraw-Hill Construction and Aviation Week. The Company has approximately 17,000 employees in 27 countries. Additional information is available at www.mcgraw-hill.com.

Follow us on Twitter: @JDPower

No advertising or other promotional use can be made of the information in this release without the express prior written consent of J.D. Power and Associates. www.jdpower.com/corporate

# # #