CS(顧客満足度)に関する調査・コンサルティングの国際的な専門機関である JD Power(本社:米国ミシガン州 トロイ)は、現地時間8月17日に、 JD Power 2023 U.S. Credit Card Satisfaction StudySM(JD パワー 2023年米国クレジットカード顧客満足度調査SM)の結果を発表した。

本調査は、年に1回、米国のクレジットカードの利用者に対して直近1年間のクレジットカード発行会社に対する満足度を聴取したもので、7つのファクターに基づいて満足度を測定している。17回目となる今回調査では、調査設計の変更が行われている。

米国クレジットカード利用者の過半数がリボ払い債務を保有

ニューヨーク連邦準備銀行によると、米国のクレジットカード債務総額は今年4月から6月にかけて450億米ドル増加し、現在1兆米ドルの大台に乗った。米国のクレジットカード発行会社にとって、この不吉な状況は、他のいくつかの消費者行動の傾向と相まって、懸念材料となるはずである。

本年調査によると、米国のクレジットカード利用者の51%が現在、平均14.8%の金利でリボ払いの債務残高を抱えていると自己申告した。クレジットカード利用者の全体的な財務状況の悪化に伴い、ロイヤルティを高めるために設定されたポイントプログラムやその他の特典に対する満足度も低下している。

2023年調査の主なポイントは以下の通り:

リボ払いとクレジットカード利用者の財務健全性の関係に注目

米国のクレジットカード利用者の半数以上(51%)が、リボ払いの債務を抱えている。この割合は、「財務的に健全でない」と分類されるクレジットカード利用者*1ではさらに増え、69%に跳ね上がる。このうち、自己申告による金利は16.5%にのぼるが、これは公表されている多くの平均値よりもまだ低い。さらに、「財務的に健全でない」クレジットカード利用者のうち、クレジットカードが支出をコントロールするのに役立っていると強く思う人はわずか11%にとどまった。

*1 JD パワーは、消費者の財務健全性を、支出/貯蓄比率、信用度、保険の適用範囲などのセーフティーネットの項目を組み合わせた指標で測定している。消費者は健全な状態から脆弱な状態までの連続的な指標において測定される。

ポイントプログラムに対する満足度が低下

クレジットカード発行会社は、より競争力のあるポイントプログラムを構築する努力を常に続けているが、「ポイント還元」の満足度は、全7ファクターの中で最も低い。これは、特にキャッシュバックカード会員において、1ドル利用あたりのポイント還元率に対する評価が低いことが要因となっている。実際、クレジットカード発行会社を変更する理由のトップは、より良いポイントプログラムを求めるためである。

最も愛されているのは年会費100ドル以上のカード

年会費100ドル以上のクレジットカード利用者は、「会員向けサービス/特典」や「ポイント還元」に対する満足度が最も高く、年会費がそれ以下または年会費無料のクレジットカード利用者よりも満足度が高い。

しかし、年会費が500ドル以上の高額なクレジットカード利用者は、提供されるポイントプログラムや会員向け特典を考慮すると、詳細評価項目の「年会費の妥当性」に対する満足度が低く、より多くの懸念を抱いている。

また、航空会社提携のクレジットカード利用者も、「ポイントプログラム」や「特典」に対する満足度は高いが、「利用条件(金利、利用限度額、手数料など)」の満足度が低く、全体の満足度向上をとどめている。

分割払いは効果的だが、利用は不安定

クレジットカードの分割払いプランを利用している顧客は、利用していない顧客と比べ、 総合満足度が+102 ポイント高い(1,000 ポイント満点)。このようなプラスの効果があるにもかかわらず、各社の分割払いプランの利用率は9%~23%まで差があるものの、全体として分割払いプランを利用する顧客は少ない。主な分割払いの利用者層は、財務的に健全な顧客か、資金繰りの困難な顧客のどちらかである。

財務的に最も脆弱なクレジットカード利用者の半数近く(41%)は、別の金融機関のBNPL(後払い決済サービス)を検討してもよいと回答した。

消費者の心に響くフィンテックの発行会社

Chime(チャイム)、Self(セルフフィナンシャル)、Ollo(オロ)などのフィンテック企業が提供する新しくて魅力的に映るクレジットカードは、従来の銀行発行のクレジットカードよりも総合満足度が一貫して高く、ブランドに対する信頼度も高い。

フィンテック企業は、若年層で、クレジットカードの債務を抱えており、ポイントを得ることよりもクレジットスコアの改善に重点を置いている顧客に特によく対応している。

JD パワー ペイメントインテリジェンス部門マネージング・ディレクター、ジョン・キャベルのコメント

「コロナパンデミックの貯蓄という余裕資金はなくなり、経済は不安定で、消費者はかつてないほど、日々の出費をクレジットカードで賄うことが多くなっている。これは、クレジットカード発行会社にとって明暗を分ける瞬間である。一般的に、高額のリボ払い債務や財務状況の悪化は、顧客の満足度やロイヤルティに悪影響を及ぼすが、クレジットカード発行会社には、分割払いプランの利用を奨励したり、好感度や信頼度を高めるためのその他の措置を講じたりすることで、顧客を支援するチャンスがある。」

顧客満足度ランキング

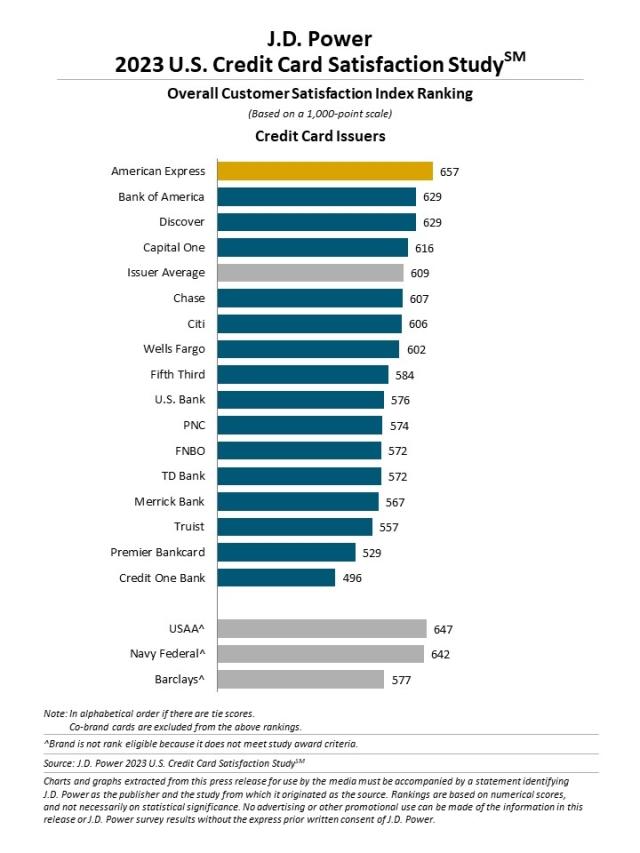

【クレジットカード発行会社部門】*2

第1位:American Express (アメリカン・エキスプレス)*3(657ポイント、4年連続の総合満足度第1位)

第2位:Bank of America(バンク・オブ・アメリカ)、Discover (ディスカバー)(同点、629ポイント)

*2有効口座数100万以上のクレジットカード発行会社(提携カードは除く)が対象。

*3 2020~2022年は旧セグメント【全国系部門】(有効口座数400万以上のクレジットカード発行会社が対象)で第1位。

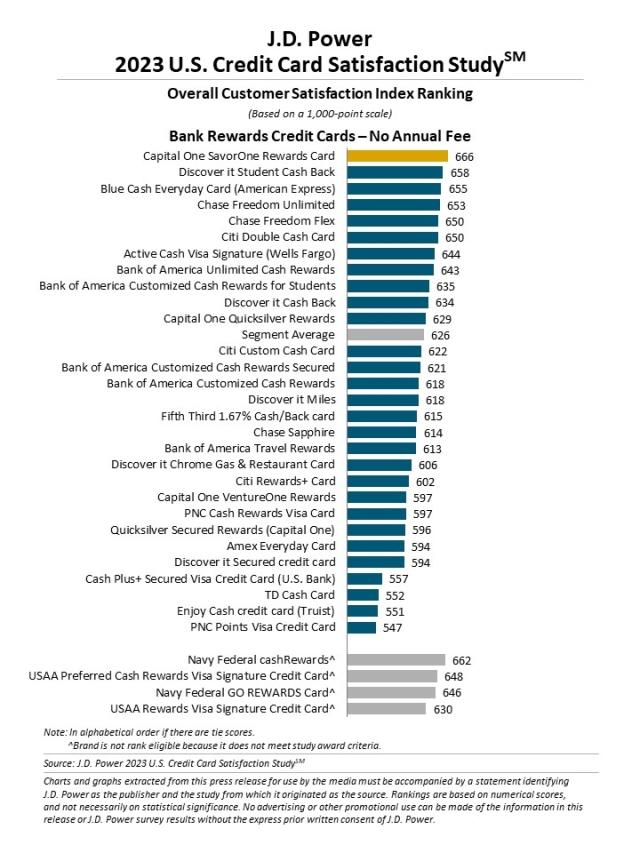

【銀行発行クレジットカード(ポイントプログラムあり/年会費無料)部門】

第1位:Capital One SavorOne Rewards Card(キャピタル・ワン・セイバーワン・リワード・カード)(666ポイント)

第2位:Discover it Student Cash Back(ディスカバー・イット・ステューデント・キャッシュ・バック)(658ポイント)

第3位:Blue Cash Everyday Card (American Express)(ブルー・キャッシュ・エブリデイカード<アメリカン・エキスプレス>)(655ポイント)

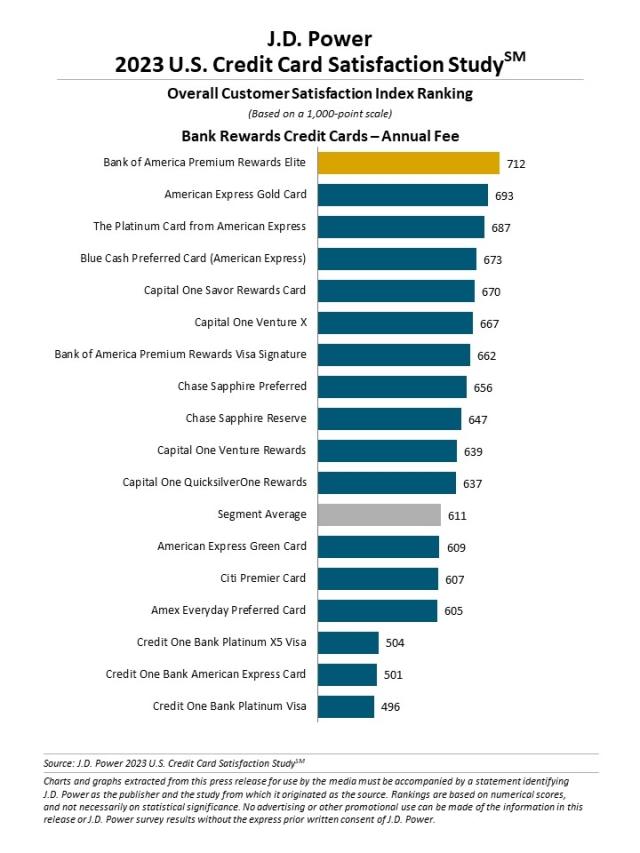

【銀行発行クレジットカード(ポイントプログラムあり/年会費あり)部門】

第1位:Bank of America Premium Rewards Elite(バンク・オブ・アメリカ・プレミアム・リワード・エリート)(712ポイント)

第2位:American Express Gold Card (アメリカン・エキスプレス・ゴールド・カード)(693ポイント)

第3位:The Platinum Card from American Express(アメリカン・エキスプレス・プラチナ・カード)(687ポイント)

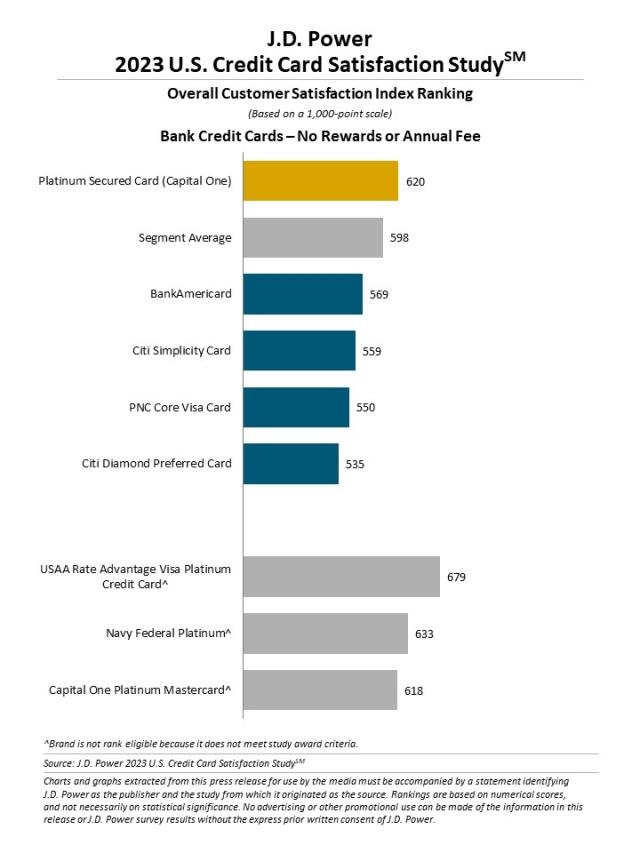

【銀行発行クレジットカード(ポイントプログラムなし/年会費無料)部門】

第1位:Platinum Secured(Capital One)(プラチナ・セキュアード・カード<キャピタル・ワン>)(620ポイント)

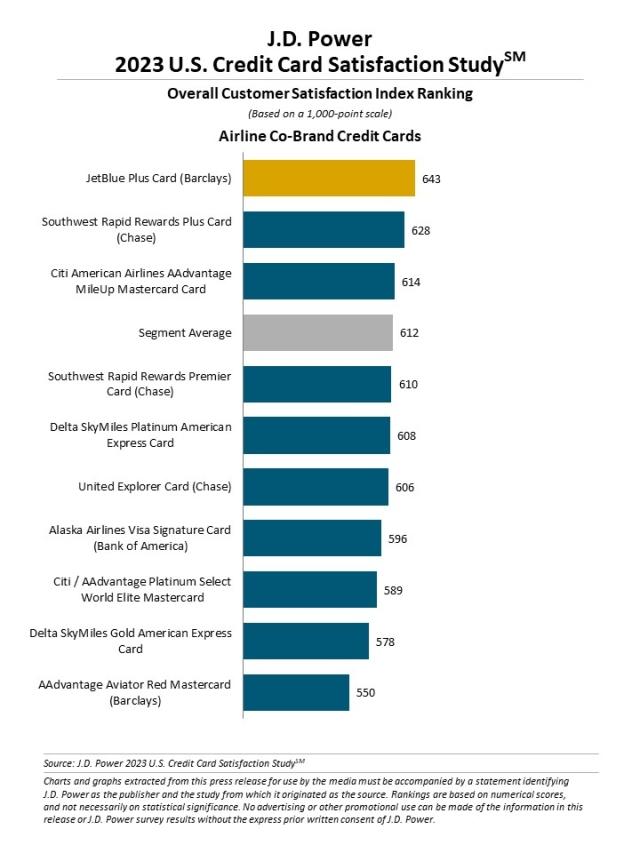

【航空会社提携カード部門】

第1位:JetBlue Plus Card (Barclays)(ジェットブルー・プラス・カード<バークレイズ>)(643ポイント)

第2位:Southwest Rapid Rewards Plus Card(Chase)(サウスウエスト・ラピッド・リワード・プラス・カード<チェース>)(628ポイント)

第3位:Citi American Airlines AAdvantage MileUp Mastercard Card(シティ・アメリカン航空・AAアドバンテージ・マイルアップ・マスターカード)(614ポイント)

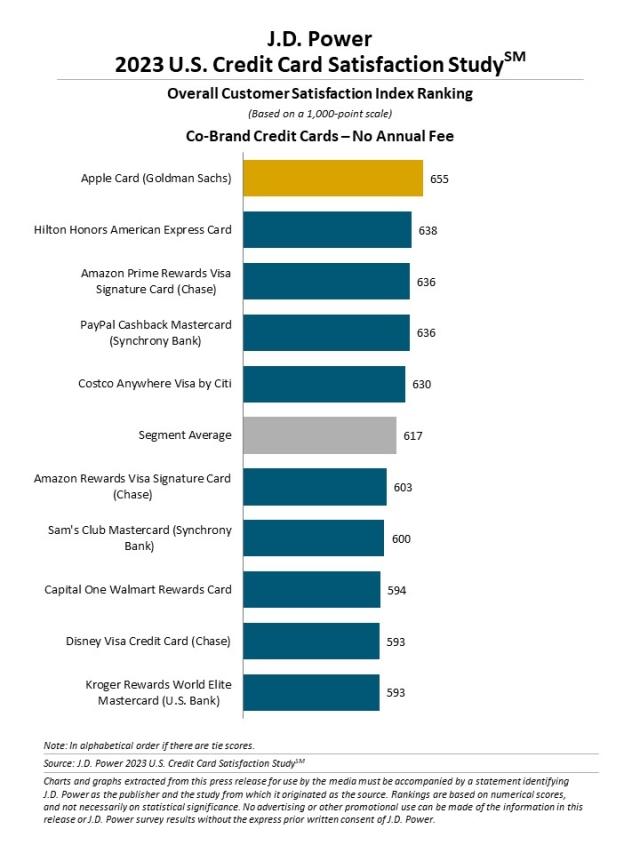

【提携カード(年会費無料)部門】*4

第1位:Apple Card (Goldman Sachs)(アップル・カード<ゴールドマン・サックス>)*5(655ポイント、3年連続の総合満足度第1位)

第2位:Hilton Honors American Express Card(ヒルトン・オナーズ・アメリカン・エキスプレス・カード)(638ポイント)

第3位:Amazon Prime Rewards Visa Signature Card (Chase)(アマゾン・プライム・リウォーズ・ビザ・シグネチャー・カード<チェース>)、PayPal Cashback Mastercard(Synchrony Bank)(ペイパル・キャッシュバック・マスターカード<シンクロニー・バンク>) (同点、636ポイント)

*4 航空会社カードは対象外。

*5 2021~2022年は旧セグメント【中規模部門】(有効口座数27.5万~400万のクレジットカード発行会社が対象)で第1位。

《JD パワー 2023年米国クレジットカード顧客満足度調査SM概要》

年に1回、クレジットカードの利用者に対して、直近1年間のクレジットカード発行会社に対する満足度を聴取し明らかにする調査。今回で17回目の実施となる。今回は調査設計の変更が行われた。

■実施期間:2022年8月~2023年6月

■調査方法:インターネット調査

■調査対象:クレジットカード利用者

■調査回答者数:31,418人

総合的な顧客満足度に影響を与えるファクターを設定し、各ファクターの詳細評価項目に関するユーザーの評価を基に1,000ポイント満点で総合満足度スコアを算出。総合満足度を構成するファクターは、総合満足度に対する影 響度が大きい順に、「利用条件」(31%)、「カード管理」(25%)、「会員向けサービス/特典」(13%)、「ポイント還元」(12%)、「ポイント利用」(11%)、「顧客対応」(4%)、「新規申込・手続き」(4%)となっている(カッコ内は影響度)。

*本報道資料は、現地時間8月17日に米国で発表されたリリースを要約したものです。

原文リリースはこちら

https://www.jdpower.com/business/press-releases/2023-us-credit-card-satisfaction-study

*JD パワーが調査結果を公表する全ての調査は、JD パワーが第三者機関として自主企画し実施したものです。

【ご注意】本紙は報道用資料です。弊社の許可なく本資料に掲載されている情報や結果を広告や販促活動に転用することを禁じます。

JD パワーについて:

JD パワー(本社:米国ミシガン州トロイ)は消費者インサイト、アドバイザリーサービス、データ分析における国際的なマーケティングリサーチカンパニーです。50年以上にわたり、ビッグデータやAI、アルゴリズムモデリング機能を駆使し、消費者行動を捉え、世界を牽引する企業に、ブランドや製品との顧客の相互作用に関する鋭い業界インテリジェンスを提供するパイオニアです。

JD パワーは、北米、ヨーロッパ、アジア太平洋にオフィスを構えています。事業内容の詳細については、https://japan.jdpower.com/jaをご覧ください。