CS(顧客満足度)に関する調査・コンサルティングの国際的な専門機関である株式会社J.D. パワー アジア・パシフィック(本社:東京都港区、代表取締役社長:鈴木郁、略称:J.D. パワー)は、2015年日本住宅ローン顧客満足度調査の結果を発表した。当調査は住宅ローンを契約している人を対象に、借入先の金融機関での経験や各種サービスへの満足度を測定している。

◆借換え需要は鈍化し、変動金利の利用が増える◆

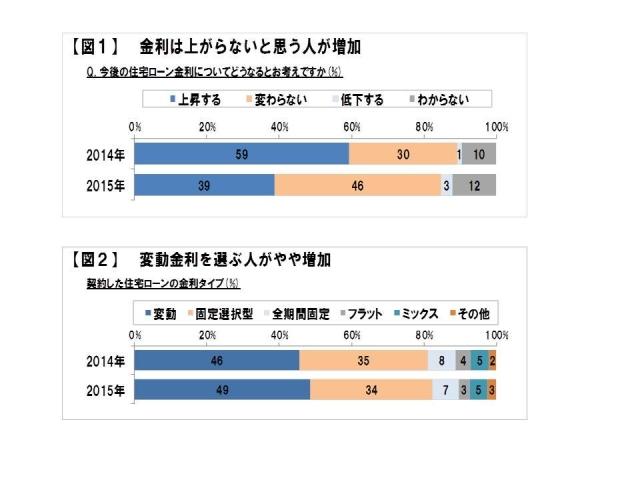

住宅ローンの金利低下が進む中、消費者の金利に対する先安観が広がっている。現在住宅ローンを借りている人のうち、今後の住宅ローン金利は「変わらない、または低下する」と答えた人は49%で、前回調査の31%から大幅に増えた。【図1】

その中、借換えの動きが鈍化している。この1年に借換えを検討したことがある人は32%と、前回から2ポイント低下した。また、直近1年の住宅ローン契約者に占める「借換え」の割合は31%で、前回から4ポイント低下している。借換えは消費者が金利上昇を意識した局面で増える傾向にある。2014年は消費税増税後に新規住宅販売が低迷した中、金利先安観の広がりで借換え需要も鈍化し、住宅ローン市場全体が冷え込んだ可能性が高い。

住宅ローンの適用金利も一段と低下した。直近1年に住宅ローンを契約した人の平均金利は、変動金利0.80%、期間固定金利1.20%、全期間固定金利1.85%で、特に変動は0.6%以下、期間固定は0.9%以下、全期間固定は1%前半が前回から増えている。

その中で、契約した金融機関を選んだ理由は「金利の安さ」がやや減り、「申込みや審査、契約手続きが簡単」「会社の知名度・信用度」が増えている。低金利競争が激化する中、消費者目線では各社の価格差が見えづらくなり、簡単、安心、といった点に決め手が移りつつあると思われる。また、金融機関を知ったきっかけでは「住宅販売会社からの紹介」「他のサービスを利用していた」が減り、「金融機関の店頭」「インターネットでのクチコミ」「住宅情報誌」などがやや増えた。消費者が能動的に住宅ローンを選び始めた兆しが見える中、各金融機関はこれまで以上に金利以外での差別化が求められよう。

一方、直近1年に住宅ローンを契約した人の金利タイプは変動金利が49%で、前回から3ポイント増えた。【図2】変動金利はこれまで東京・大阪近郊や大手企業勤務者に多い傾向だったが、この1年では中京圏や中小企業勤務者、年収が高くない人など、これまで固定金利を選ぶことが多かった人でもその利用が増えている。

変動金利は返済負担が少ない反面、金利上昇に伴う負担増のリスクを消費者が負うことになる。その点を十分考慮して契約したのであればよいが、借入れの際に複数の返済プランを検討した人は34%で、前回の43%から減少しており、金利の先安観を背景に一部安易に変動金利を選んでいないか危惧される。消費者も金融機関も、これまで以上に金利リスクを意識して、慎重に金利プランを選定することが必要だと思われる。

◆堅調に成長してきたネット銀行も、借換え中心の成長は頭打ちの兆し◆

ネット銀行の住宅ローン取り扱いは2002年に始まり、その後、シェアを着実に伸ばしている。今回調査は8%となった (シェアは契約者数ベース)。その強みは、金利や手数料の安さにあるが、加えて、課題であった審査期間が長い点も、この1年で改善しており、契約時の満足度も向上している。また、借入れ後も繰り上げ返済のサービスなどを中心に評価が高く、メインバンクとして利用される割合も増えており、住宅ローンを契機にした顧客の囲い込みは進んでいる。

一方、これまでネット銀行の成長を支えてきたのは借換え市場だが、金利の先安観が広がる昨今、借換え中心での成長は難しい局面になったといえる。過去数年に比べて、この1年のシェアの伸びも鈍化した。一部のネット銀行は、住宅販売会社やファイナンシャルプランナーの紹介を通じ、新規の住宅購入客を獲得しているが、今後もネット銀行が成長するには新規客の更なる開拓は必須だといえる。

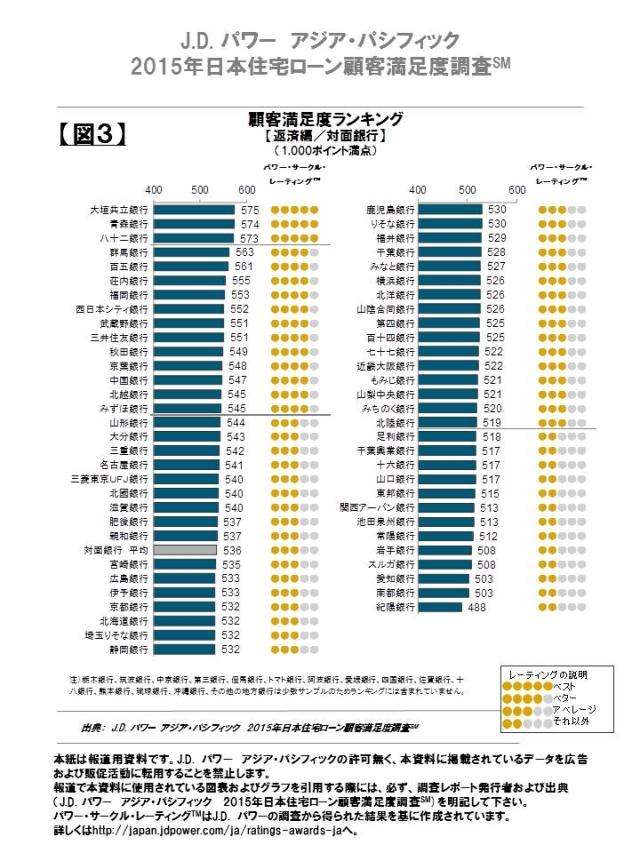

◆大垣共立銀行、ソニー銀行が顧客満足度1位◆

対面銀行 部門(対象60行)【図3】

大垣共立銀行が1位となった。同行は「各種案内/手続き」がトップ評価で「店舗施設」の評価も高い。2位の青森銀行、3位の八十二銀行は「各種案内/手続き」と「顧客対応(担当者)」の評価が高い。

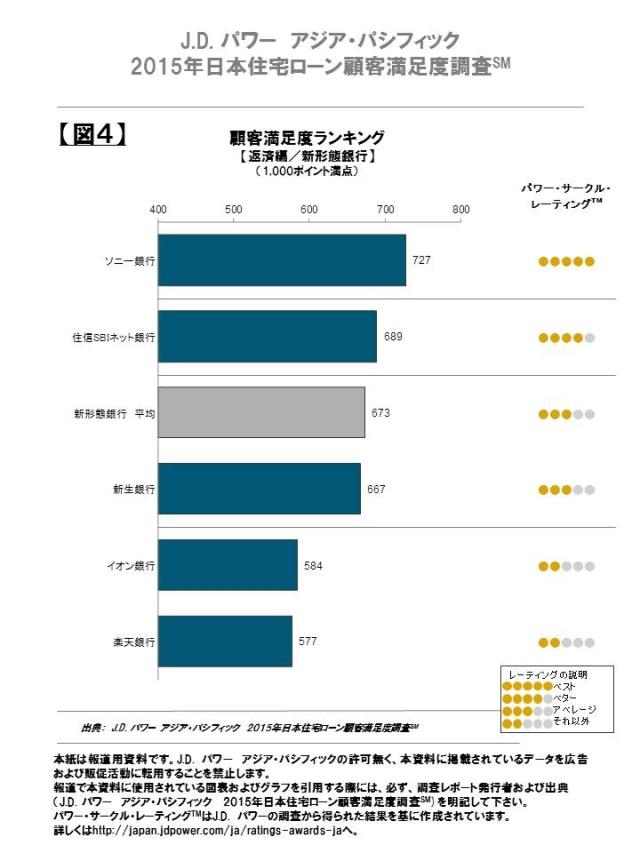

新形態銀行 部門(対象5行)【図4】

ソニー銀行が1位となった。同行は「各種案内/手続き」「顧客対応」でトップ評価を得ている。2位の住信SBIネット銀行、3位の新生銀行は「各種案内/手続き」の評価が高い。前回同様、大半の金融機関は契約後の満足度は低下するが、ソニー銀行、住信SBIネット銀行、新生銀行の3行は契約後の満足度が上昇している。

<調査概要>

当調査は住宅ローンを契約している人を対象に、借入先の金融機関での契約時や返済時における経験、各種サービスへの満足度を調べたもので、全国20歳以上の男女を対象にしている。また、直近1年以内に住宅ローンの新規借入か借換えを行った人を【契約編】、契約して1年以上経過している人を【返済編】として集計している。本年調査は、2014年11月にインターネット調査を実施し、16,914人から回答を得た。(契約編:5,137人、返済編:11,777人)

【返済編】の満足度測定は、3つのファクター(要素)を設定し、各ファクターの総合満足度に対する影響度をもとに総合満足度スコアを算出した(1,000ポイント満点)。各ファクターの影響度は高い順に「各種案内/手続き」が68%、「顧客対応(担当者・オンライン・コールセンター)」が21%、「店舗施設」が11%となっている。

また、当調査ではサービス形態をもとに「対面銀行」「新形態銀行」の2部門に分けて集計した。なお、信託銀行やコミュニティバンクも参考データとして聴取している。

※対面銀行:都市銀行、地方銀行 ・新形態銀行:ネット専業銀行、その他銀行

※信託銀行:信託銀行 ・コミュニティバンク:労働金庫、信用金庫、信用組合、JAバンク

<金融業界関連の当社発表調査>

※日本住宅ローン顧客満足度調査:2014年より開始。住宅ローンを契約している人が対象の満足度調査。(当調査)

※日本投資サービス顧客満足度調査: 2012年より開始。銀行、証券会社の個人投資家が対象の満足度調査。本年は7月に報道発表予定。

※J.D. パワーが結果を発表する調査はすべてJ.D. パワーが第三者機関として自主企画により実施したものです。

<株式会社J.D. パワー アジア・パシフィックについて>

当社は米国J.D. パワーの日本を含むアジア地域でのビジネス拠点として1990 年に設立された。自動車業界を始め通信、IT、金融、トラベルなど様々な業界において顧客満足に関する調査やコンサルティングを実施している。尚、J.D. パワーではシンガポール、北京、上海、バンコクに拠点をもち、日本、オーストラリア、中国、インド、インドネシア、マレーシア、フィリピン、台湾、タイ、ベトナムで調査を実施している。会社概要など詳細は当社ウェブサイトhttp://japan.jdpower.comまで。